America's Obsession: Keeping up with the Debt

September 10, 2022

Happy Saturday Wolves! I have to say this article is going to be a little longer, but it has a lot of information and data that I think you may find very interesting. If you want the TL;DR just skip down to the conclusion where I summarize the findings, make some predictions, and rant on Jerome Powell (Yes, again I know but you have to admit this guy is asking for it!) Alright, without further ado, let’s jump into it.

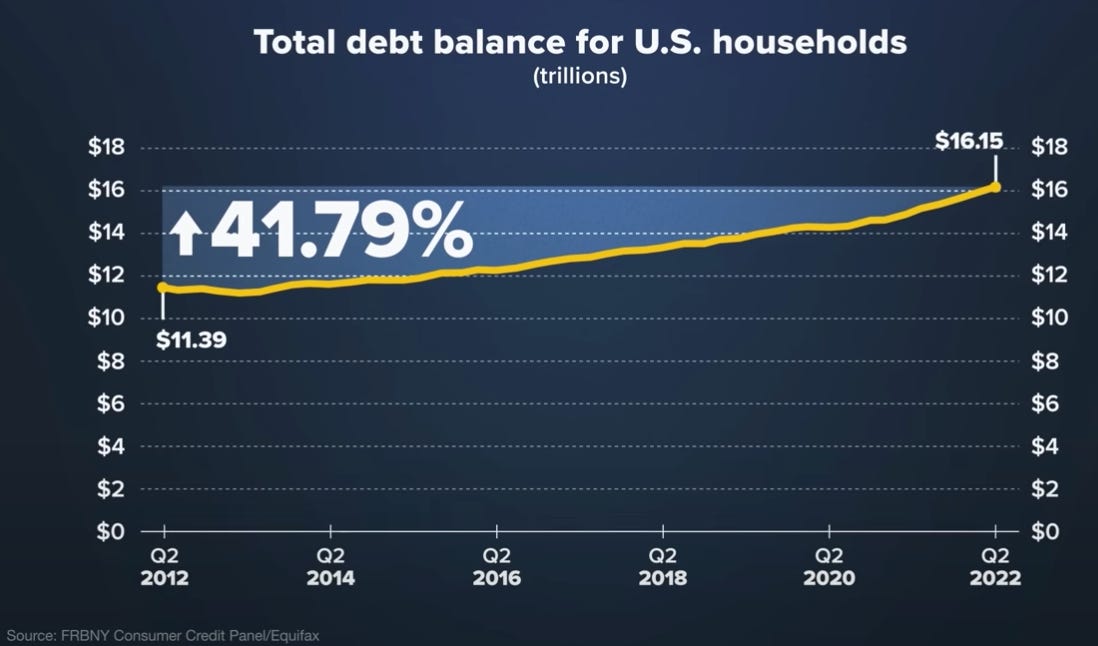

America has an obsession. No, I’m not talking about the Kardashians, relax. I’m talking about debt. We love it and just can’t seem to get enough. However, 2008 showed us the perils of over-lending. That recession taught us many valuable lessons that flew straight over the heads of most people in charge of this country. If you’ve been keeping up with debt, you’ll notice we always find a way to delay the problem. Whether it’s congress consistently raising the debt ceiling or more recently Biden “canceling” student debt, we invent new ways to continue pushing it to the side. Since it hasn’t been an imminent threat for well over a decade now, the issue has fallen off the radar for most people. Nonetheless, debt has been silently growing in the background by 41% in just the past decade.

However, let’s get one thing straight. Debt is not necessarily a bad thing. It is what allows us to scale our businesses, purchase our homes, and finance our education. Debt only becomes an issue when the asset that is backing it up is in trouble. So, to understand our exposure to higher debt levels, we need to assess the health of our assets. If you know your accounting 101 principles, you’ll know that Assets = Liabilities (Debt) + Equity. Your equity represents your net worth or wealth. You can increase your equity with income or when the assets that you own appreciate in value. When you want to make a big purchase of a home, for example, you have the price of the asset (house) that you will purchase most likely using a mix of equity and debt. Your equity or principal payment here is fixed at the time of purchase. So, if you lower your borrowing costs, liabilities go down and thus asset prices must increase in order to balance the equation. On the other hand, if the cost of borrowing goes up, asset prices must decrease.

This is how we understand the important relationship between the cost of borrowing and the price of assets. It’s basic intuition that somehow often gets overlooked. My very first article criticized the Fed’s decisions throughout the pandemic because they drastically manipulated the money supply and lowered interest rates to near zero unnecessarily and for way too long. That’s why we have inflation levels we haven’t seen in over 40 years and asset bubbles all over the place thanks to the extremely low costs of borrowing. If you haven’t read that article yet, you can find it here. Today, Jerome Powell and the Fed are trying to reverse course in a desperate attempt to tame the inflation beast that they woke up. They are doing this by raising interest rates which raises the cost of borrowing for everyone. This will inevitably bring asset prices back down, but the pace at which this is done is very important to nail that “soft landing” everyone is talking about.

That’s why I believe Jerome is overestimating the financial health of consumers and of our economy for that matter. Why? Well, the reasoning goes like this: Printing artificial money lowers the cost of borrowing which artificially inflates assets. Artificially inflated assets then make people artificially wealthy (Equity). With increased equity, you can take on more debt to purchase more inflated assets. However, this debt is definitely real, and by no means artificial. What happens when those artificially inflated assets come back down to reality? The debt remains unchanged and unphased, so your equity must come down in order to balance the equation. See the problem? People have less equity than they think they currently have, which makes them more exposed to debt than they even know. However, is this the situation that we find ourselves in today? Let’s dive into this great pool of American debt, shall we?

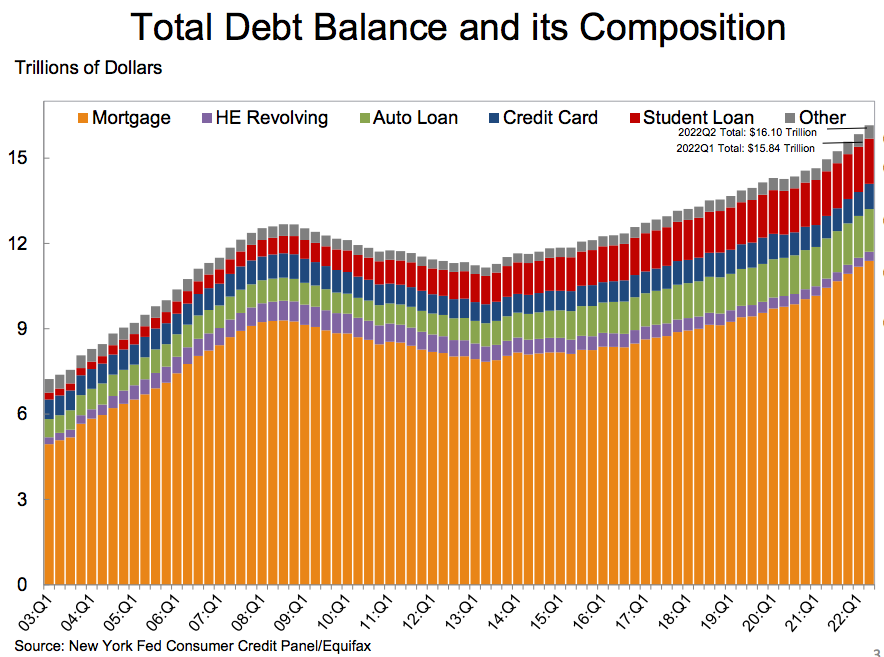

First, let’s see what household debt looks like currently in America. We can break down our debt into 4 main categories: Housing, student loans, credit cards, and auto loans. From the graph below we can see that housing makes up the majority of our debt at 72.5%. 10% is student debt, 9% are auto loans, and 5% is credit card debt.

Our debt levels are sitting at an all-time high of $16.10 trillion, $2 trillion higher than it was in the fourth quarter of 2019. In just the second quarter of 2022, we increased household debt by $312 billion.[1] That’s a pretty big number for just 3 months of the year. But like I said, debt isn’t necessarily a bad thing, it just depends on the assets and equity that are backing them. So, let’s take a look at some new Q2 2022 data that can give us some insights to see how the average American consumer is doing.

Housing:

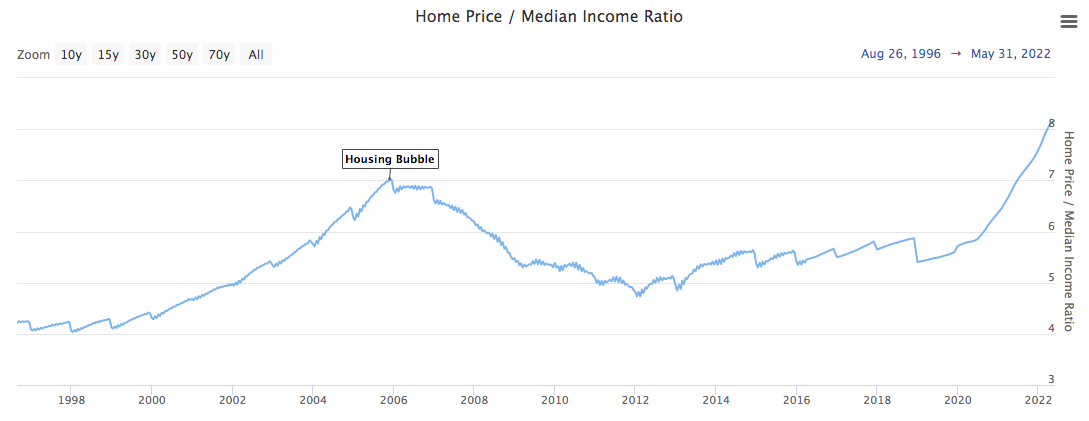

Let’s start with housing since it is the biggest component of household debt. It’s no secret that home prices are out of control right now. In fact, homes have never been more expensive than today. Not even in 2008.[2]

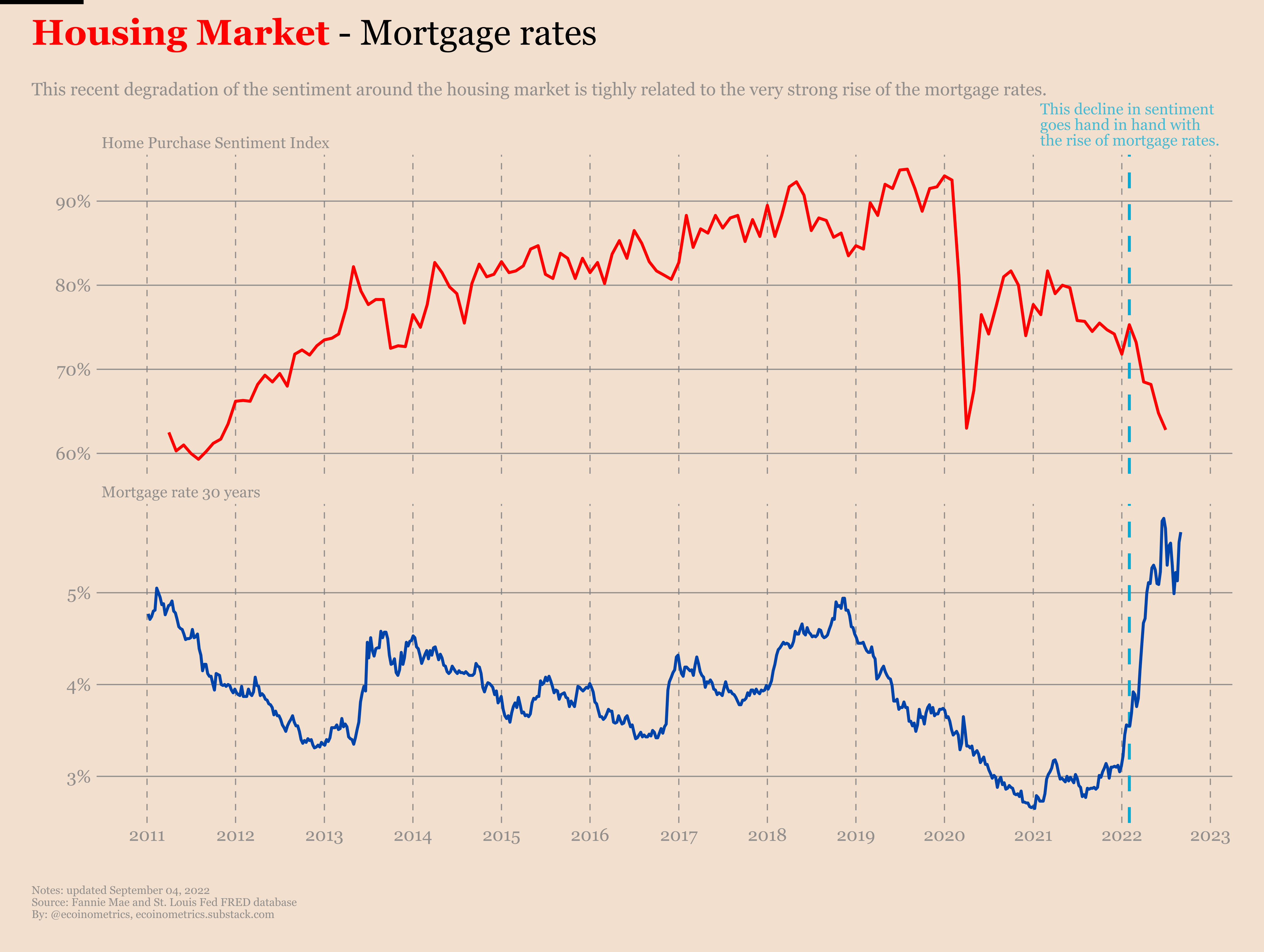

Home prices rose sharply during Covid due to high demand led by cheap debt and rising construction costs. Now with mortgage rates increasing, prices are finally starting to plateau. However, if we want to get the most up-to-date information on the real estate market, we need to look at the right data. Median home prices are not ideal because this is a lagging indicator by about 60-90 days due to closing times and reporting methods. Let’s take a look instead at some leading indicators that can tell us where the market is going next. For example, the Home Purchase Sentiment Index is a good indicator of future demand trends from home buyers. Most home buyers do not buy using all cash, they normally require some sort of financing. So, it is no surprise that demand will be strongly linked to mortgage rates. The graph below shows this relationship. Again, let’s take note that as the debt for purchasing a home becomes more expensive, demand for homes decreases.

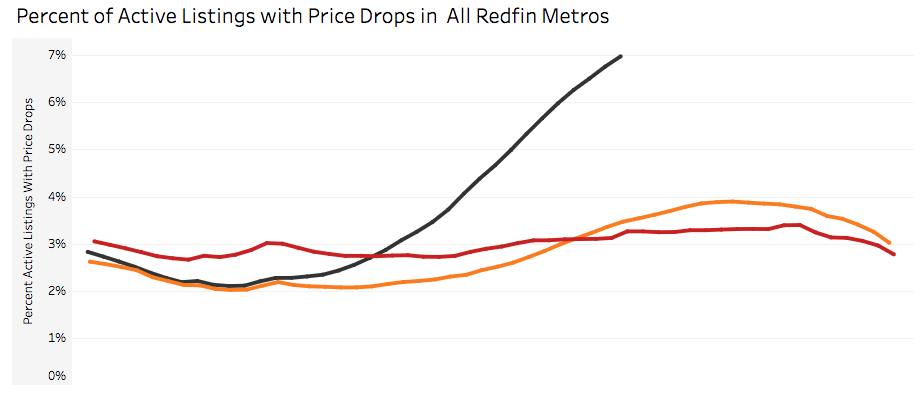

Now let’s take a look at another leading indicator: price drops for active listings. Redfin is a very popular, nationwide, real estate brokerage that publishes key data insights on a weekly basis. In the chart below, the red and orange lines represent 2020 and 2021 respectively. The black line represents the ongoing trends of 2022. As you can see, the percentage of active listings that have dropped their asking price has more than doubled in the past few months.

It would be no surprise if housing prices make a U-turn later this year. This will reduce the equity of most homeowners throughout the country and have big implications on the average consumer’s financial health.

Student Loans:

Now let’s look at student loans. Biden recently extended the student loan freeze for a fourth time until January 2023. He says this is the final extension and I actually believe him this time because I don’t think he’ll care as much after the midterm elections honestly. A survey by a pro-student debt cancelation organization found that 93% of their members said that they are not ready to restart their loan payments.[4] However, we’re definitely going to need to take this number with a grain of salt. Given this group’s interests, we can probably assume a degree of bias to push their agenda forward.

Nevertheless, the former FDIC Chair, Sheila Bair, concurs. She said that “borrowers aren’t ready…Borrowers haven’t had to make payments for well over two years. Their budgets have come to rely on not making those payments and you’re going to see some massive non-payment and delinquency rates go up and hurt credit scores. The longer they're in non-payment status, the harder it is to get a borrower to start paying again. This is one of the things we learned during the financial crisis when we were trying to get mortgage borrowers with reduced payments to start repaying their loans.”[5] Right after she made those comments, Biden announced his new student loan proposal extending the payment freeze another 6 months.

When payments eventually do restart in January it will be almost three full years since they have been frozen. According to a recent Equifax study, the average monthly student loan payment ranges between $244-$393.[6] That’s quite a big number for a majority of people in this country. Will people be able to quickly incorporate this added expense into their budgets? We won’t know until 2023, but with the cost of living shooting up, I wouldn’t want to take that bet.

Credit Cards:

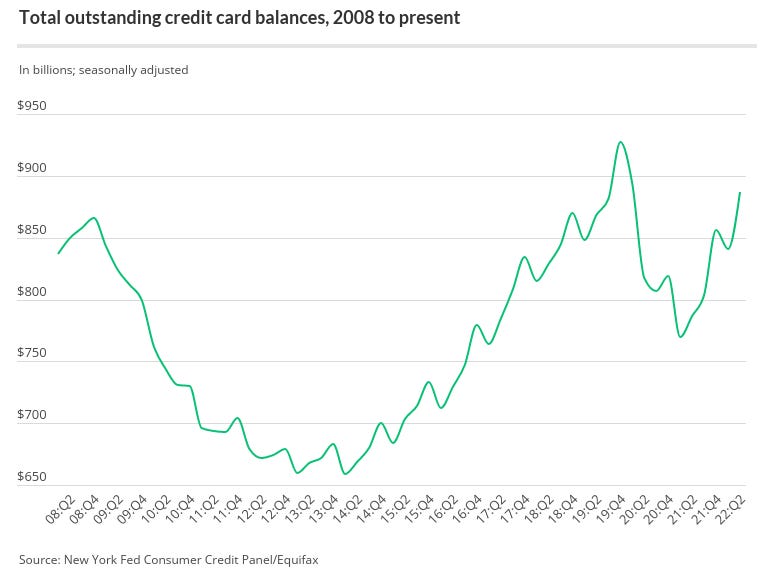

Talking about the cost of living, let’s take a look at credit card debt. According to the Federal Reserve, about 80% of adult Americans have at least one credit card so it’s a good way to measure how people are doing financially. Pandemic stimulus gave people a chance to pay off a lot of their credit card debts as we can see from the graph below.

It fell from $927 billion in the 4th quarter of 2019 to $770 billion in the first quarter of 2021. However, since the fourth quarter of 2021, it has started to shoot back up, right around when inflation picked up. This trend has obviously persisted since expenses continue to climb with credit card balances rising by $46 billion just this past quarter marking the largest year-over-year increase since 1999. [7]

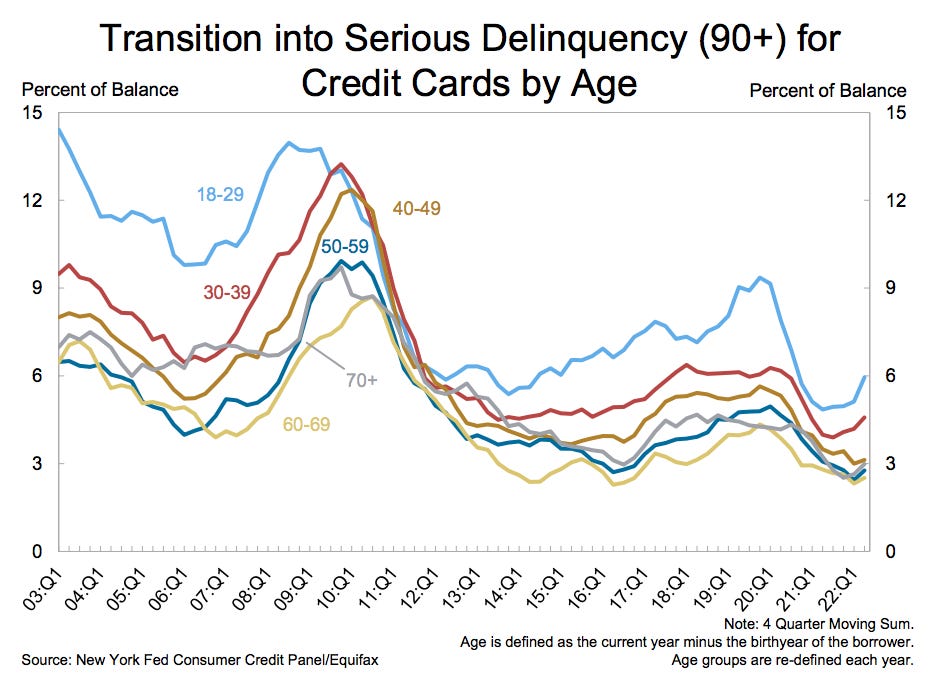

Now let’s take a look at the graph below showing delinquency rates on credit card balances. This is still relatively low compared to pre-covid levels and especially in 2008. However, it’s the newest data from Q2 of 2022 that is starting to tell a new story. A sharp spike upwards for almost every age group, especially for young people. (You know the same people who hold the most student debt) Interestingly enough, delinquency rates were also dropping until a year before the 2008 crash when they also started shooting up. While Q2 provided new information on consumer health, we still need to wait to see how fast things progress next few months before jumping to drastic conclusions though. Nevertheless, the current pace at which we are taking on new credit card debt isn’t good news for the health of the American consumer.

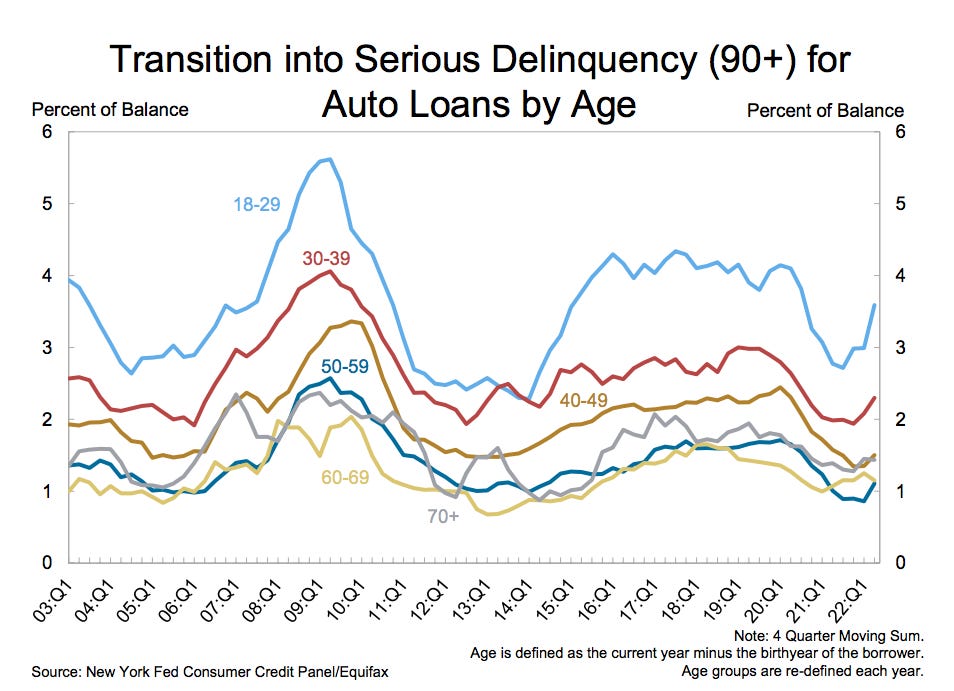

Auto loans:

I wrote about auto loans and the used-car market a little over a month ago. In that article, I showed how the used-car market is in a bubble largely thanks to the federal reserve making debt so cheap, which allowed car lenders to lower borrowing standards drastically. This led to a 40%+ spike in used-car prices and has led to 30-40 million people overpaying for their cars. Auto debt is also more dangerous than home debt because cars are a naturally depreciative asset while homes tend to be the opposite. I end that piece by saying that used-car prices will drop by around 30% once they go back to normal levels and we can expect delinquencies to rise a great deal as well. If you want to check out that article, you can find it here.

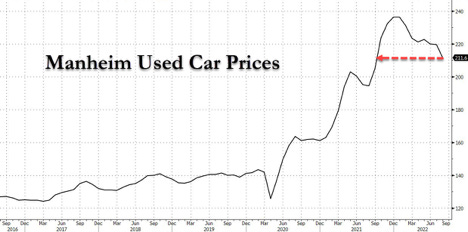

Now that we have access to Q2 data, the predictions above are starting to come true. Used car prices have now dropped to a new 1 year low. The world’s largest wholesale auto marketplace, Manheim, posted this graph below to show the trend.[8]

This past month’s slump was the largest since April 2020. Furthermore, if we want to look at real-time data, “Sell my car” google search jumped 222% according to a study by findthebestcarprice.com.[9] Now let’s look at the graph below showing auto loan delinquencies.

Yup, this is also spiking in Q2. With the Fed raising rates and crushing demand, these trends will only endure. Used-car prices will continue to fall sharply in the next few months which reduces the equity levels of millions of Americans.

Conclusion:

So, what have we learned so far? Household debt has reached an all-time high of $16.1 trillion. A majority of that debt is tied to mortgages for homes that are over-valued and expected to fall in value due to sharply decreasing demand. Student loan borrowers are seemingly unprepared to restart payments in January. Credit card debt and delinquencies are increasing thanks to inflation and are expected to continue rising. Finally, the used-car market bubble is popping and the tens of millions of Americans with auto loans will be deeply affected. All these trends in tandem will be reducing the equity for a majority of Americans in the months to come.

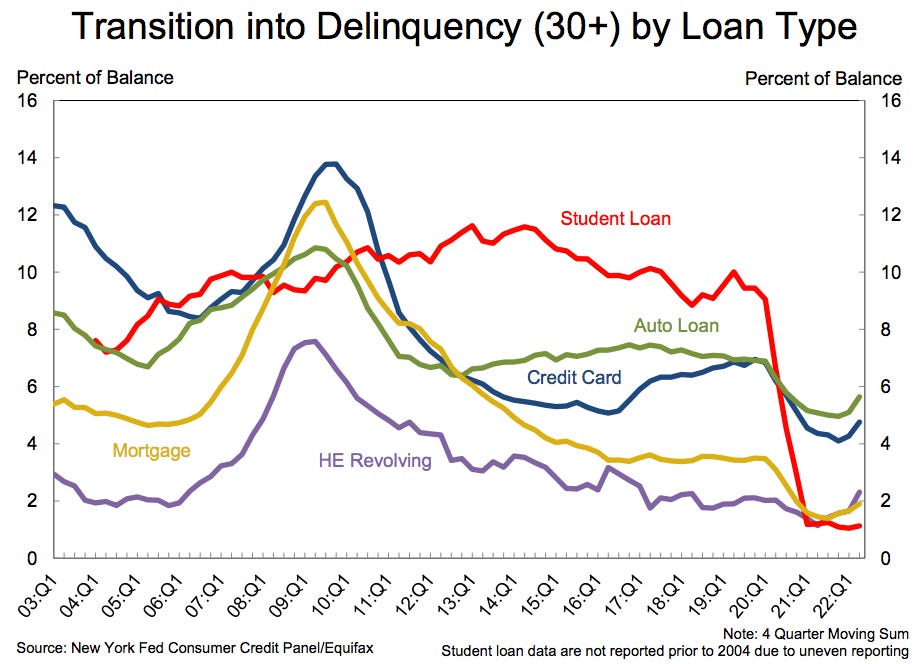

I’m just going to leave one more chart below to sum it all up by loan type:

As you can see, the delinquency rates are still below pre-pandemic levels, which is why this is not a talking point in mainstream news, yet. However, it is the sharpness of the increase in Q2 data that should be worrisome because Jerome Powell is not on track to make that “soft-landing” happen.

So if you’ll allow me, I’m just going to go finish with a quick rant on Jerome Powell here as he is the culprit behind all of this, and I anticipate he’s only going to aggravate the situation in the next few months. Let’s start by retracing his steps since the pandemic:

- Jerome caused the highest inflation levels seen in over 40 years by artificially printing $4.7 trillion in 2 years. Less than a year ago he was calling it “transitory” remember?

- He created asset bubbles by maintaining low-interest rates for way too long. The low cost of borrowing inflates asset prices. We’ve seen this story play out with university tuition, cars, real estate, and basically anything you can put a price on.

- Funnily enough, Powell still blames Covid-19 for inflation.[10] Either he is completely unaware of basic economic principles or he is lying to the people to cover his ass. You choose.

- Now, in a last-ditch attempt to dampen the inflation that he started; he is following his predecessor Paul Volcker’s playbook that created the highest unemployment rate since the Great Depression, destroyed small businesses and the working class, and even started a massive debt crisis in Latin America.

The Fed is now set to raise rates again in their next meeting on September 21st. The current debate is whether to raise rates by 0.5% or 0.75%. A small difference with massive implications. Powell is unaware that most assets are currently overpriced and is more unaware of how raising rates too quickly could cause a devastating domino effect. If asset prices across the board fall too fast, then that can create a panic-sell situation since the rational consumer will want to cash in their remaining equity before it continues to drop. The “soft landing” everyone is talking about is having asset prices decrease at a slow steady rate. The data we have seen from Q2 screams anything but steady. Sharp increases like we are currently seeing and expecting from Powell will lead to the crash landing that everyone wants to avoid.

So, there you have it, folks. We will need to see how things continue to unfold in the next few weeks and I may be updating this article every couple of months when there’s new data to keep you informed. The truth is though that Jerome Powell has backed himself into a corner and the only way out now is the Paul Volcker way of making everyone poorer. Volcker’s legacy is complicated because he came to office during an extended period of high inflation. He is praised for managing to tame the raging inflation but also criticized for devasting millions of Americans in the process. Jerome is different, he came in during the longest economic boom in American history, but will now be responsible for creating a lasting recession thanks to his careless decision-making. He may very well go down as the worst Fed Chairman in all history.

Sincerely,

The Canny Wolf

[1] https://libertystreeteconomics.newyorkfed.org/2022/08/historically-low-delinquency-rates-coming-to-an-end/

[2] https://www.longtermtrends.net/home-price-median-annual-income-ratio/

[4] https://studentdebtcrisis.org/student-debt-covid-19-survey-5/

[5] https://finance.yahoo.com/news/student-loans-resume-payments-165818941.html

[6] https://www.equifax.com/resource/-/asset/presentation/resource-market-pulse-the-impending-student-loan-impact-for-young-borrowers-webinar-slides/

[7] https://libertystreeteconomics.newyorkfed.org/2022/08/historically-low-delinquency-rates-coming-to-an-end/

[8] https://www.zerohedge.com/markets/used-car-market-cools-prices-plunge-year-low

[9] https://www.findthebestcarprice.com/when-will-car-prices-drop/

[10] https://www.ibtimes.com/fed-blames-pandemic-inflation-hopes-soft-landing-will-it-happen-3611209

Printing money is like a cancer....don't we have enough examples in many other countries? Argh!