Consequences of the Fed: The Auto Bubble

August 5, 2022

While the Ancient Greeks are no longer around, their culture and philosophies still influence us to this day. In fact, one of my favorite aspects of their society was their ability to tell great stories. That’s because each story incorporated morals and lessons that are applicable throughout all of human history, which is probably why they have stood the test of time. There’s one I’ve been thinking about recently that I feel is particularly reminiscent of our current times. It is the story of King Midas. For those who aren’t as familiar with the tale, King Midas was a very wealthy ruler obsessed with money. One day the gods granted him a wish and he asked that everything he touch turn to gold. The gods warned King Midas of the potential consequences, but the King dismissed their concerns and proceeded anyways. At first, he was delighted that he could take an ordinary object and inflate its value tenfold with just a simple touch. However, he quickly discovered how little he knew about his powers and accidentally turned his food and even his own daughter into solid gold. Having realized his gift has turned into a curse, King Midas hoped his new power would simply be “transitory”. However, he soon found out that this was not the case and desperately tried to reverse course…see where I’m going with this yet?

Yes, Papa Powell is King Midas in this situation. Back in 2020, Powell wished for $4.8 trillion in stimulus money and, despite many warnings, he got his money. At first, everything seemed…golden. 2021 was like Tom Brady vs Atlanta Falcons in Super Bowl LI. The economy came back stronger than ever with the S&P 500 hitting all-time highs 68 different times.[1] That’s roughly 1/3rd of all trading days in the year. Everywhere you looked people were making money in stocks, real estate, and even Bitcoin for god sake. However, it wasn’t long before things that we didn’t want to turn into gold did.

In my last article, I show how the Fed’s monetary policy is the real underlying cause of the inflation we are seeing today. However, inflation isn’t the only consequence that the Fed’s policy has on our economy. When the Fed bought trillions of dollars worth of bank securities, they also lowered something known as the IORB rate dramatically. IORB stands for Interest on Reserve Balances. The official definition is the “rate of interest that the Federal Reserve pays on balances maintained by or on behalf of eligible institutions (i.e. banks) in master accounts at Federal Reserve Banks. The interest rate is…an important tool of monetary policy.”[2] This rate is crucial because it dictates how banks assess new loan originations. When the IORB rate is near zero, banks are desperate to put this cheap cash out in the economy because at the Fed it’s earning them almost nothing. On the other hand, when the IORB rate is higher (i.e. 5%) banks need to be pickier with their lending standards. They must ensure the loan provides them a minimum 5% return because if not, they’d be better off parking their money at the Fed.

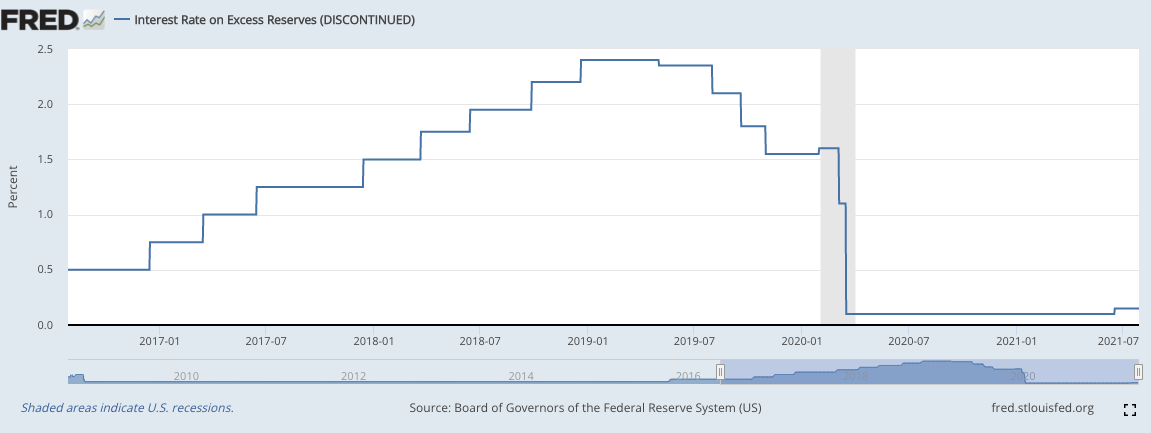

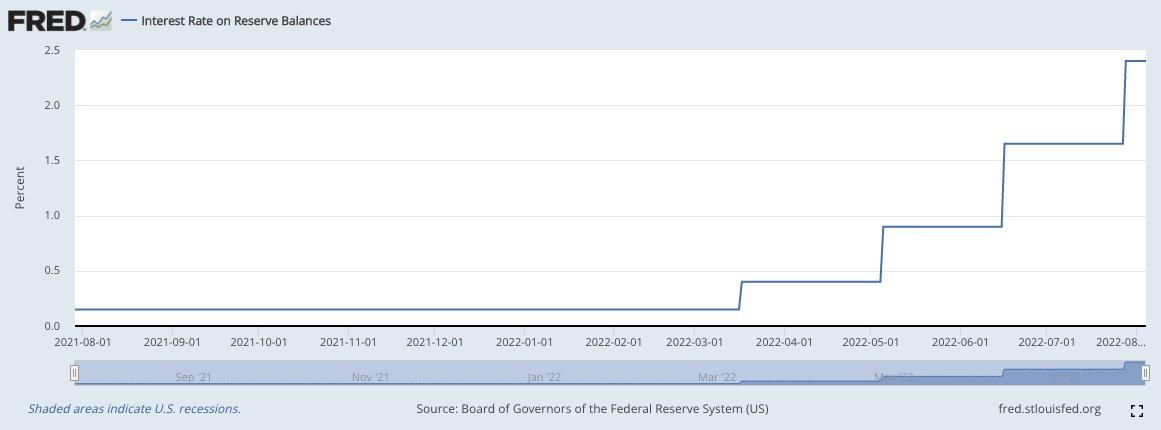

Above are the graphs of the IORB rate since 2017. It’s two separate graphs because the IORB rate went through a name change in mid-2021, however, it is the same interest rate. You can see in the first graph how the IORB rate dropped on March 16, 2020 to 0.10%[3], effectively nothing. The rate was raised slightly to 0.15% in mid-2021. It wasn’t until inflation was slapping us in the face when Powell finally decided to raise IORB rates again to the 2.5% mark.

When the Fed lowers the IORB rate to near zero, they incentivize banks to issue far more loans. Banks no longer need to ensure that their investment will be fruitful, they just need to beat the 0.10% return that they’d get at the Fed. It’s also important to note that the lending risk for banks is also dramatically lowered, but not for the borrower. Should the borrower default on a loan, the bank has collateral they can take to recover their principal investment. If the collateral is still not sufficient, they can also sue in most cases to take other personal belongings of the borrower in order to meet their demands, such as houses, cars, etc. While banks prefer you to succeed so they can charge more interest, they are not worse off should you fail when the IORB rate is near zero because there is no opportunity cost anymore. In this situation, the house always wins.

Let me provide an example. Imagine the IORB rate is lowered to near zero and banks are desperate to lend out their cash. In their desperation, they give everyone’s grandmother a loan to start a cookie business and they say may the best G-Ma win. In this scenario, the grannies with the worst cookies will go out of business, end up in default, lose their homes, and go straight to the bad nursing homes; you know the ones with the most Covid infections. (Too soon?) Meanwhile, my grandma with the best cookies will be running a small cookie factory in no time. In either situation though, the bank still wins. My grandma paid back her principal plus interest while nursing home ‘Meemaw’ used her house as collateral, so the bank fully recovered their investment on her too. Now imagine if the IORB rate was at 5%. Banks would’ve needed to be more careful now because should the borrower default, they’ll lose out on the 5% they could’ve earned by just letting the cash sit with the Fed. Perhaps in this scenario, they would’ve tasted each grandma’s cookies and only lent to the one with the best batch. My grandma would still have her factory and your grandma would still have her house.

Okay enough with the abuelas, where do we see this actually happening today? Well, we need to look no further than our garages because the used-car market is quite literally off the charts. If we look below, we can see used-car prices have jumped by 42.4% from 2020 to 2021. By comparison, new car prices have increased by 11.6%.

What has led to this drastic increase in car prices? I’ll first present the factors that most outlets are pointing to. Let’s flashback to 2020 when Fauci’s lockdowns began. Driving decreased substantially because most people had nowhere to go and were working from home. However, with the vaccine rollout in early 2021, businesses opened back up, kids were allowed back in the classrooms, and offices adapted to hybrid schedules. Driving came back in full force. Many people also received Uncle Sam’s stimulus check, which increased their disposable income. Finally, auto factories experienced global chip shortages, staff shortages, and low inventory which meant a scarcity of new cars in the market. To sum it all up: demand came back faster than expected, supply was hindered for a myriad of reasons, and people had excess savings and stimulus money to spend. Doesn’t this story sound familiar to most other industries? Yes, we’ve seen price increases across the board, but a 40%+ spike should tell us something else is going on…

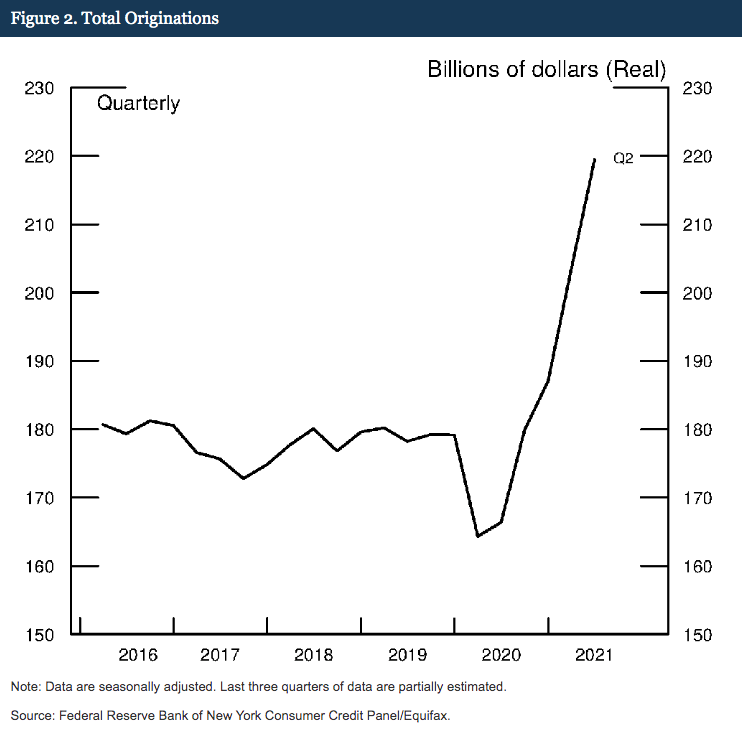

Perhaps it was Powell’s Midas touch that cursed the used car market? Let’s take a look at this graph below depicting new loan originations in the auto market.[5]

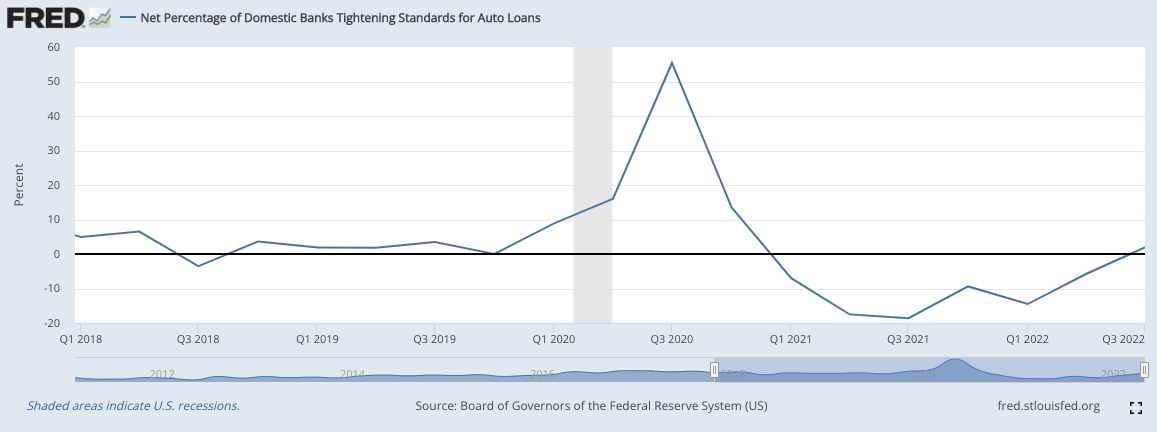

As you can see, when the pandemic started, banks freaked out and slowed down lending. However, as soon as Papa Powell lowered that IORB rate, the banks weren’t just going to let their cash sit idly by at the Fed. They were desperate to get that money out and into the hands of consumers as fast as possible. In order to do so, they had to lower their lending standards to allow more people to qualify for loans. Below is another chart showing the percentage of banks tightening their standards specifically for car loans. As soon as that IORB rate dropped, so did their pants…I mean, lending standards.

Only now that the IORB rate is finally going back up so are their zippers. Nevertheless, this led to some wild lending parameters last year. Typically, auto loans have a loan-to-value (LTV) ratio of about 60-80%. However, in 2021, borrowers were getting LTV rates of up to 140%.[6] This means that if you want to buy a $10,000 car, the bank would give you $14,000 to pay for it. Yes, I know this makes no sense. However, the bank can charge more if the loan is bigger. Remember, they need to move the most cash they can out of the Fed and into the hands of borrowers, and they don’t really care if the borrower will be able to pay it back or not. That’s why we see in 2021, 96% of borrowers didn’t even have their income verified when they applied for their auto loan. [7] This over-financing done on a broad scale is why the used-car market is the way it is today. Yes, the supply constraints played a role in limiting new car inventory and pushing consumers towards the used-car market. Stimulus checks were also a nice boost that gave people the confidence to spend more in the short term. But the 42.4% spike in prices was really caused by the Fed pushing the banking system to take advantage of and over-inflate the used-car market.

Current Outlook:

Today, 83% of people are currently overpaying for their cars.[8] That’s compared to only 2.8% a year ago, and 0.3% two years ago. These trends are troubling and clear indicators of a bubble. We see this in the housing market too, however, there’s an important difference. Cars are depreciating assets: the more miles you put on your car the less it’s worth. Homes, on the other hand, tend to appreciate in value over time. What makes this worse is that once automakers stabilize the supply of new cars again, used car prices are expected to go back down by ~30% to ‘normal’ levels. Furthermore, they won’t be able to refinance to a new loan with lower payments since interest rates have gone up and may not come back down for years to come.

By the time prices normalize, 30-40 million used cars will have been sold to consumers for about 30% higher than they should have paid. When these same consumers come in to trade their cars at normal prices a few years from now, they will have little to negative equity to fund their next purchase. This will surely create a drag on the auto market for years to come.

Conclusion:

By lowering IORB rates to near zero, the Fed incentivizes risky lending habits that can lead to the creation of bubbles, especially in markets that experience supply and demand shocks. The Fed needs to establish a minimum IORB rate to ensure that banks always have an opportunity cost because reckless lending standards take advantage of the unwitting borrower. The used-car market is a clear example of this and in the next couple of years, we’re going to see a sharp increase in auto loan delinquencies and repossession rates. Borrowers will be left with tainted credit scores and reliant on our overcrowded and underfunded public transportation systems. Too many American families and businesses will be put in jeopardy for the ineptitude shown by our Fed officials.

The story of King Midas ends with him pleading to the gods to take back his gift. They accept and tell the King to go to a nearby river to wash off his golden powers. He follows their instructions and when he returns, he finds his daughter alive and healthy. Perhaps we should try throwing Chairman Powell into the Potomac river as well. If that doesn’t make inflation magically disappear, it would at least teach him a lesson because the Fed seems to be blissfully unaware of the consequences of their actions.

[1] https://www.reuters.com/markets/asia/live-markets-sp-500-puts-another-record-high-close-under-tree-2021-12-23/

[2] https://fred.stlouisfed.org/series/IORB

[3] https://www.federalreserve.gov/newsevents/pressreleases/monetary20200315a1.htm

[4] https://advisory.kpmg.us/articles/2021/used-car-prices-could-crash.html

[5] https://www.federalreserve.gov/econres/notes/feds-notes/delinquency-rates-and-the-missing-originations-in-the-auto-loan-market-20220211.htm

[6] https://www.barrons.com/articles/recession-cars-bank-repos-51657316562

[7] https://www.consumerreports.org/car-financing/many-americans-overpay-for-car-loans-a8076436935/#:~:text=By%20spring%202021%2C%20an%20estimated,of%20New%20York%20and%20Philadelphia

[8] https://www.edmunds.com/industry/press/8-out-of-10-of-car-shoppers-paid-above-sticker-price-for-new-vehicles-in-january-according-to-edmunds.html