The U.S. Recession and Inflation of 2022: How We Really Got Here

July 28, 2022

Today, the US Bureau of Economic Analysis released its estimate of GDP for the second quarter of 2022. As most economists predicted, this number was negative. Thus, by definition, the U.S. economy has entered into a new recession (no matter what propaganda the White House uses to change the definition). We have had four recessions in the 21st century and each one has had a clear culprit. In the early 2000s, we saw the spectacular collapse of the dot.com bubble. In 2008, the subprime mortgage crisis collapsed the housing market. Finally, in 2020, the pandemic lockdowns fleetingly halted economic activity across the world. Now in 2022, inflation is soaring to records that most Americans only ever read about in Econ 101 textbooks. Nevertheless, the true cause of today’s economic woes appears to be suspiciously unclear with both sides of the aisle pointing at different reasons. And yet, the real culprit has been hiding under our noses this whole time. That’s right… it’s the Federal Reserve.

The growing theme of incompetent leadership in this country continues, and this time we can find it in the most powerful financial institution in the world. The unnerving hubris showed by the Fed in recent years is the main reason we currently face 40+ year inflation highs. To fully understand why we should all be calling for Jerome Powell’s head on a stake, we need to go back a few years to see how we got into this situation in the first place.

Background:

It was after the 2008 recession when the Fed first applied the policy of Quantitative Easing (QE). For those who didn’t major in economics in college but wished they did, QE is a form of monetary policy that the Fed uses to increase the supply of money in order to spur economic activity. They do this through large-scale purchases of bank securities to provide banks with more cash, which in turn makes the banks more inclined to issue new loans. QE worked pretty darn well from 2009 to 2014; it slowly but surely pulled us out of the Great Recession and into the longest boom in our entire economic history.

However, it is important to note that there is a second consequence of Fed monetary policy that is often underestimated. That is the psychological effect of the Fed’s guidance on the markets and public perception. See, Wall Street loves nothing more than the Fed saying, “I got you,” when times become…well, unprecedented. That’s exactly what happened at the beginning of the COVID-19 pandemic. Flashback to March 2020 when the world entered into strict lockdowns due to the uncertainty of this new virus. Economic activity halted and the stock market tanked by over 30% in the span of a week. So, Papa Fed put on his hero cape and stepped in with a warm bowl of QE soup to tell us everything will be alright. And this is the exact moment where we need to start paying attention.

On March 23, 2020, the Fed announces that they will be using “its full range of tools” (a.k.a. QE) to heroically save us from our economic woes. The very next day, the market was up almost 5% and it never looked back from there. Wall Street proceeded to go on an outstanding bull run for the next 20 months with the S&P 500, Dow Jones, and Nasdaq all reaching record highs never seen before. Then in Dec. 2020, the Fed indicates that they will actually be increasing QE by $120b more per month and will only consider changing course once they determined that we have fully recovered from the March 2020 crash. However, the stock market had already reached its previous all-time high by Sept. 2020. Somehow, record-setting housing and stock markets combined with record low unemployment in early 2021 apparently also didn’t meet Jerome’s “tiger parent” expectations.

The Fed continued its course despite clear indicators that the economy was overheating throughout 2021. Consumer spending was through the roof, company valuations were higher than ever, and home prices nearly doubled across the country. It all just seemed too good to be true. Yet nobody cared to bat an eye because hey, look around dumbo, we’re all getting rich right? Nevertheless, the question remained: what really influenced this unbelievable rebound and appreciation in asset prices? Perhaps everyone decided to remodel their kitchens and increase their homes’ square footage by 50%? Maybe every major company found a magical way to improve profitability overnight? Ah, or maybe it was the fact that the Fed poured trillions of dollars into the economy and relayed messages of overconfidence to the public for months on end in their forward guidance? Papa Fed and his warm bowl of QE soup were here to stay.

It wasn’t until Nov. 2021 that the Fed finally decided to start tapering off its asset purchases, but that was way too little and way too late. Reading that press release now makes you want to laugh and cry at the same time. Here are some notable anecdotes from the report: “The Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent.” I wonder if our current 9% inflation was what they meant by moderately above 2%? Here’s another: “The path of the economy continues to depend on the course of the virus. Progress on vaccinations and an easing of supply constraints are expected to support continued gains in economic activity and employment as well as a reduction in inflation.” For the Fed to call attention to Covid vaccinations as a factor in taming inflation truly underscores their lack of understanding regarding inflation – and the vaccine, for that matter.

The Facts:

This is where we get to the core of the issue of the Federal Reserve. See, QE had never been attempted prior to 2008 and was controversial amongst several economists who noticed its potentially dangerous consequences. The concerns were valid, but the issue in 2008 was that commercial banks’ balance sheets had taken massive hits due to these subprime mortgages. Their ability to make new loans and create money was seriously impaired. QE at that moment made sense, especially since interest rates had already been cut to near zero. The Fed heeded warnings and implemented the new policy at a moderate pace. After all, it was our first experience using QE. The recovery was slow but steady, and eventually, the turtle won the race. QE was seen as an overall success.

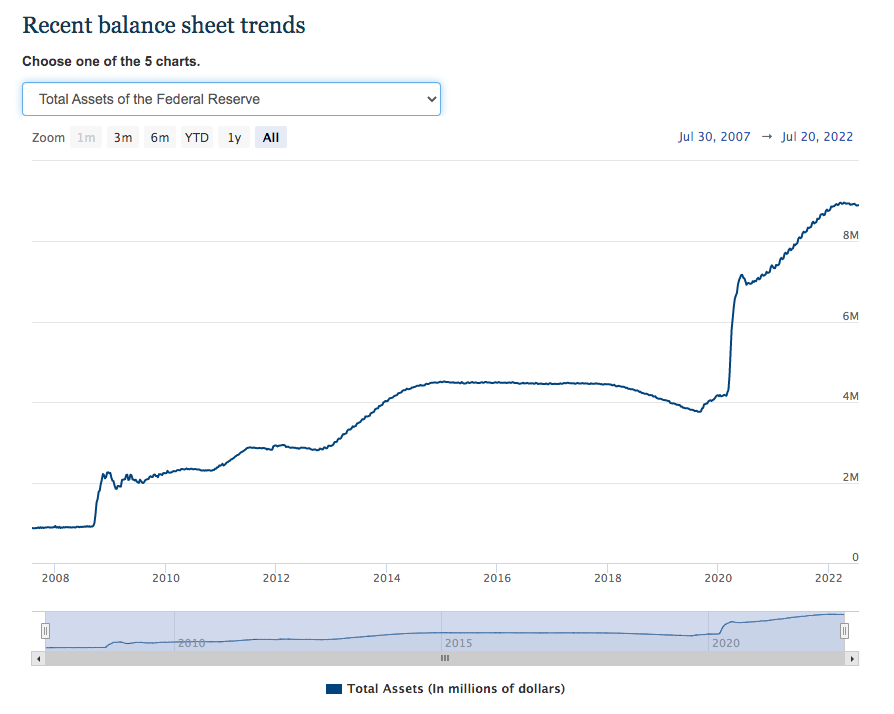

However, like most drugs, the first experience is wonderful and addicting, and the next time around you want to try even more. If the Fed is a low-income white from rural Pennsylvania, QE is its opioid. Before 2020, the Fed had implemented QE policy three times: first in 2009, then again in 2010, and the third time in 2012. If we take a look at the Fed’s balance sheet, we can measure how many drugs (liquidity) the Fed was pumping into the economy’s veins.

In the first round of QE, dubbed “QE1,” the Fed bought about $1.75 trillion in mortgage-backed securities, agency debt, and long-term treasury securities from March 2009 to March 2010. In QE2 near the end of 2010, the Fed purchased an additional $600 billion over the course of almost a year. Then in QE3, the Fed continued purchasing securities from September 2012 to October 2014 for a total of $1.67 trillion total. In August 2007, before the financial crisis hit, the Fed’s balance sheet totaled about $870 billion. By January 2015, after those large-scale asset purchases had occurred, its balance sheet swelled to $4.5 trillion.

While this may sound like a lot of money to you, those are just rookie numbers for Jerome “the tank” Powell. If you’re looking at the graph you might be wondering about that border wall size leap in 2020. If you didn’t already know, Jerome Powell is like the Walter White of money printing. From the original announcement in March 2020, the Fed increased its balance sheet by a staggering $2.9 trillion in a matter of three months. Riding this high, Mr. Powell continued to purchase an additional $1.8 trillion in securities. Today, the Fed balance sheet sits at a whopping $8.9 trillion.

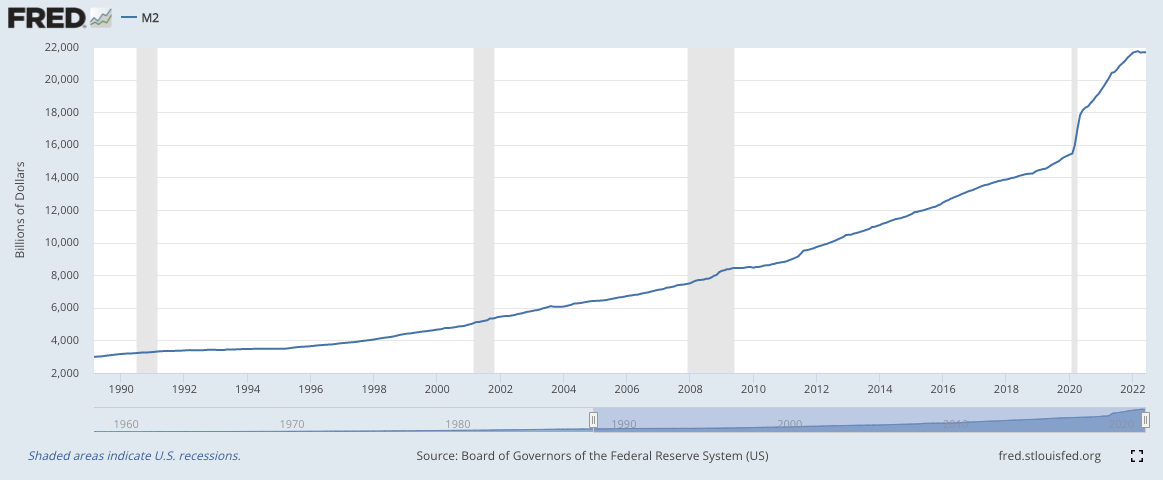

Economists in 2008 sent many warnings that adding this much liquidity into the system could cause runaway inflation, and yet it never did. So how do we really know that this is what is actually causing the inflation we are seeing today? The current right-wing narrative tells us it was those socialist policy stimulus checks given out freely to the people that caused them to stop working and disrupt supply chains. The Left disagrees and says the supply-chain issues are caused by the unvaccinated, corporations practicing “greedflation” and the Russia-Ukraine War pushing energy prices up worldwide. These are all reasonable factors to consider if we were bleating sheep believing everything Fox News and CNN have to say. Fortunately, some of us can think for ourselves and we have to look no further than the M2 money supply to see why Jerome has failed all of us.

Why M2? M2 is important to look at because it measures the twofold effect of the Fed’s monetary policy and forward guidance. It takes into account not only the asset purchases of the Fed but also the money created from commercial banks’ lending. Again, the Fed’s goal and guidance at the start of the pandemic was to encourage banks to lend more and continue stimulating what was already a strong economy. This is the combination of the market operations and the psychological effect that the Fed has on the economy.

Let’s take a look at the graph above tracking M2 money supply. M2 has been growing at a constant pace for several decades now and it hasn’t been particularly affected by economic booms or busts. However, the first slight discrepancy we can see is in 2009, when QE1 was first implemented. It’s a noticeable bump if you happen to have a magnifying glass handy. Now let’s look at 2020. Quite the difference, right?

The actions the Fed took increased M2 by 41% in 2 ½ years and yet we still debate why we have record-high inflation. It shouldn’t be a surprise that when you increase the supply of money by that much, you are going to wake up the inflation beast. QE is a powerful tool that can be used for good, but we can’t deny that it pokes the sleeping bear that is inflation. While it worked in the past and the bear stayed in its hibernation, this time Jerome basically punched the bear straight on the nose. Yet he has the audacity to blame a tight labor market and a war on the other side of the world. What is more frustrating is that so few people are discussing this fact - but I can’t be surprised when both parties love to say anything but the truth.

We should be holding the Fed in more contempt because it should have been obvious that this was going to happen. The economy in 2008 was very different from the one we had in 2020. In 2008, we were in a bubble. Prices of assets were over-inflated, banks were over-extended, and the economy was simply overvalued. At the start of 2020 however, we were in the middle of the longest economic boom in history. Production had never been higher, unemployment was near all-time lows, and inflation was below 2%. When COVID-19 finally hit, our economy was Arnold Schwarzenegger strong. This is where I believe our society fell victim to media fearmongering about the virus. Now, I do believe a good degree of caution was needed, especially at the beginning when we had no concept of the potential severity of COVID-19. Nevertheless, we need to remind ourselves that the media profits off of our fears and anger, all while politicians tend to love more power and control. The officials at the Fed were no exception and, like all of us, they too overreacted to the situation. The Fed took an already hot economy and decided to inject $4.8 trillion of additional liquidity into the system without a second thought.

The only economist I’ve seen that has been talking about this is Prof. Steve Hanke from the Johns Hopkins University. Prof. Hanke states that in the Fed’s “panic to raise rates and begin quantitative tightening, the Fed has, in the three months before June, allowed M2 growth to plunge to an anemic annualized growth rate of 0.1%. When broad money growth falls to near zero, nominal spending contracts and a recession begins.” Thus, the Fed has forced themselves into a bind with no escape. They can either trigger a recession in the hopes to kill the inflation and the working class along with it or continue M2 growth at a moderate pace and risk inflation entrenching itself into consumer expectations. Either option will hurt, and I just hope Jerome Powell and the rest of the Fed don’t Houdini their way out of accountability for their mistakes.

Conclusion:

The Fed seems to be power-drunk on the immense responsibility and influence that they have over the U.S. economy and economies across the globe. The psychological impact alone of their guidance is a very real thing and, if misused, has tremendous consequences. They voluntarily decided to take it upon themselves to not only calm investor fears but to incentivize increased investment and spending. After the longest economic boom in history, they were arrogant and overconfident in their abilities to manage monetary systems. They used their guidance to shift market expectations and create a bubble of false confidence for investors and consumers alike.

While I am not particularly against the use of QE, the Fed made our economy overdose on its effects. What’s worse is that they had ample opportunities to call in the medics throughout all of 2021, but they didn’t. Now they are scrambling to reverse course, but the damage has already been done. The level of incompetence displayed by our alleged best economists at the Federal Reserve troubles and saddens me. We have just entered a recessionary period for the fourth time this century no matter how Powell, Yellen, or Biden try to spin it. Whether we start feeling it now or in a few months doesn’t matter. The bear is awake and is already hurtling towards us.

Sincerely,

The Canny Wolf